As many of you, it was that time of year to make sure I had my health insurance figured out for 2019.

My employer doesn’t offer health insurance benefits so it’s something I take care of on my own. That’s okay with me because it gives ME control of what kind of health insurance I want or need. It’s my health insurance and I should know what I need, right?!

Before choosing a plan:

So there are a few things about health insurance one needs to become familiar with prior to comparing plans.

Copays: a fixed dollar amount you pay each time for a certain type of care. For example: $25/ doctor visit. Many of us are familiar with this one.

Deductible: a amount you must pay for most insurances begin to pay. Beware: the deductible may not apply to all services so check over your plan. Again, many of us are familiar with deductibles, specially with other insurances we have. KEY: The higher the deductible, the lower the premium.

Coinsurance: your share of cost of a covered service calculated as a percentage. For example: 20%/80% = you pay 20% of the bill and your insurance would pay 80%. This breakdown kicks in after the deductible is met.

Common breakdowns I’ve seen are 20/80 and 30/70. This is one not everyone is familiar with and it doesn’t really tell you an actual dollar amount it’s going to cost you. KEY: The lower your share, the higher the premium.

Out-of-pocket-max: The most you have to pay for health services during the year. The out-of-pocket maximum includes your deductible, copays, and coinsurance. This can get over looked, when people focus more of their time looking at the other items above.

What I look at in choosing a plan:

Most people would consider lower copays and 20%/80% better than a 30%/70% plan with higher copays, right?

I only look at 1 number when I compare plans and that is: OUT-OF-POCKET-MAX -aka what is the most this is going to cost me in a year?

To me, the other items of fluff and mean little to nothing to me.

Difference in plans out there:

Let’s play with some numbers. 🙂

Example of a Typical Health Insurance Plan: Premium $250/month – $3,000/year

Copays: $30/doctor visits, $40/urgent care, etc

Deductible: $3,300/member

Coinsurance: 30%/70%

Out-of-Pocket-Max: $7,300/member

Example of a Non-typical Health Insurance – HSA APPROVED: Premium $160/month – $1,920/year

KEY: Member is to pay bills in full until deductible is meet

Deductible: $6,700/member

Coinsurance: n/a – after deductible is meet, insurance covers in full

Out-of-Pocket-Max: $6,700/member

Okay, hold up! What is an HSA?

A HSA is a health saving account. Think of it as an emergency fund just for your medical bills. 🙂

Now we got that out of the way….

Which plan would you chose?

Which plan would give you good coverage for the cost?

Let’s walk through the examples as I follow Dave Ramsey’s philosophy (cover the small stuff and transfer the risk of the big stuff to the insurance companies).

Typical Insurance: Total premium is $3,000 + $7,300 = $10,300 maximum potential total cost for a year

Non-tropical Insurance: Total premium is $1,920 + $6,700 = $8,620 maximum potential total cost for a year. A SAVING OF $1,680.

So why aren’t more people getting HSA approved health insurance?

Great question! Who wants to pay $1,680 MORE if they are hospitalized?! Not me. If I’m hospitalized, I have bigger problems to be concerned with, right?!

The kicker with HSA approved health insurance follows Dave Ramsey’s philosophy in that, YOU are responsible to cover the small stuff (doctor visits, minor medical care, etc) while transferring the risk of the big stuff (hello! being hospitalized, surgery, etc) to the insurance companies.

Taking on some risk up front, drills down the yearly premium, which is what you want too. Take that money saved in premium and put in into your HSA account.

But the HSA approved health insurance deductible is so high!

$6,700 is a lot for a single mom to dish out, but remember it’s also the Out-Of-Pocket-Max number too! That’s huge!

AND if you are like me, only really using the health insurance to cover something major, you won’t need to use the HSA account often, therefore it’s going to start building up. YESS!!!

The goal is to have your Out-Of-Pocket-Max saved in your HSA account along with some extra cash as a cushion for random medical bills that come in. The amount of the cushion would be the amount you feel comfortable with having in there.

For example, by the end of 2018, I will have almost all of my deductible saved. 😀

Talk about peace of mind! And if I get sick and need to see the doctor, I’m not worried how am I going to come with the max-out-of-pocket money in my tight budget to pay for it. I just write the check. Simple as that.

Before you dump your savings into your HSA….

The government limits how much you can put into a HSA account so make sure you are following those requirements.

So per the IRS, 2018 limit was $3,450/year.

(Math time again! WHOOHOO!!!!!) 😀

I had set up automatically, $40 to come out of my checking account (after I got paid) to be transferred into my HSA savings account. That would be $1,040 ($40 x 26 paychecks) for the year. So I had room to add more money to my HSA account so today I transferred an additional $2,000 from my saving to my HSA saving. (Don’t worry, I’m going to hustle to replace that $2,000 ASAP!) 😉

Why contribution (deposit) the limit or close to the limit year year? Well, currently (not sure if what the new tax changes will be in the future), I am able to take what I contributed to my HSA for that year and DEDUCT it off my income when I do my tax return PRIOR to the standard deductions, etc (since I am using after tax-dollars to fund my HSA.

Other things to know about HSA’s:

1. You can’t pay your premiums from this account

2. Your health insurance HAS TO be HSA approved to be able to have a HSA account.

3. Any deductions have to be a medical expense and the monies in the HSA account can only be used for such.

Okay, okay, okay. Why am I so passionate about HSA’s and health insurance?

So yeah, I’m slightly passionate about the topic. Not only do I save money throughout the year via lower premiums, I have built up a saving in my HSA which give peace of mind if something major happens, and I get a tax benefit at the end of the year via my tax return.

Need another reason?!?!……

Why I feel having an HSA and choosing the right health insurance is SO IMPORTANT?

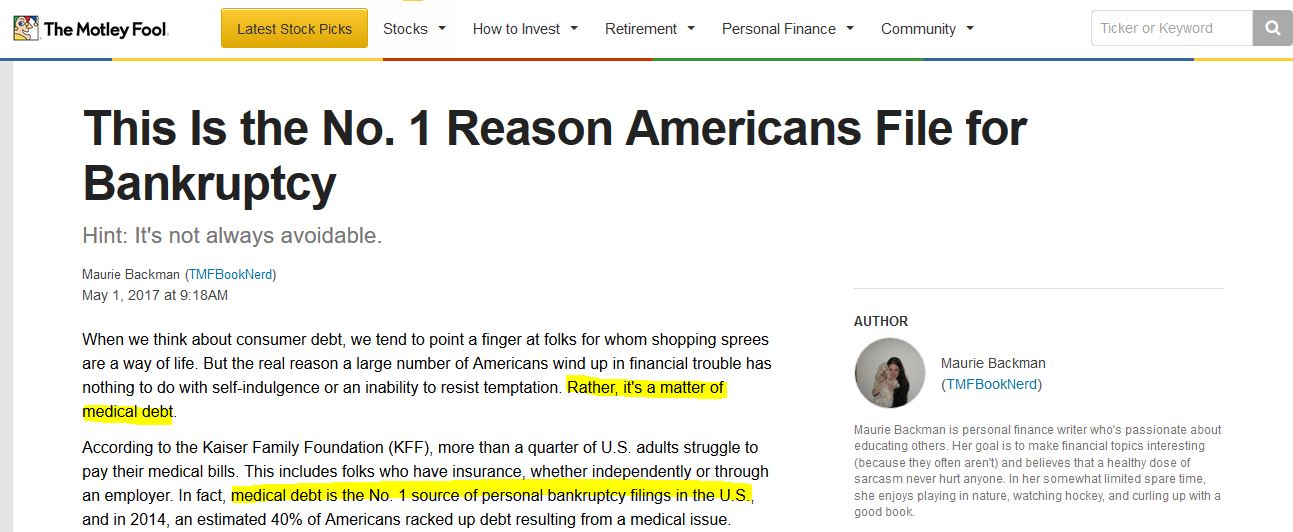

THE #1 REASON AMERICANS FILE FOR BANKRUPTCY IS NOT CREDIT CARD DEBT BUT MEDICAL DEBT.

Let that sink in for a moment……….

So when you are building wealth, you don’t want to lose it all and your financial stability over one incident when you find yourself in the hospital.

As Dave Ramsey says, cover the small stuff and transfer the risk of the big stuff to the insurance companies.

![20180702_073425[1]](https://hazelreflection.wordpress.com/wp-content/uploads/2018/07/20180702_0734251.jpg)